That Once In A Life Thing... What Credit Card Should I Use For Wedding?

The other day, husband and I were looking at redeeming our miles for our much delayed honeymoon. With a sigh, I realised quickly that this will probably be the only time I am ever taking a business class flight given how little (thankfully) we spend each month.

He said to stop dreaming about it ever again because the main reason why we had so many miles was because of our expenditure for the wedding and house combined. I asked if I can marry him again lol. Or must I marry a new guy? Hmmm. Anyway, savvy spenders are usually split into two main groups of card users - one who prefers miles, and another cash back.

I was/maybe am still a firm believer of cashbacks because back when I was using the Manhattan card, miles weren't a popular choice so, options were limited. Also I was able to get the $200 quarterly rebates easier since it was 5% cash back and now Standard Chartered nerfed it -,- I am considering to go back to a cash back card soon, since we rarely spend over $500 a month (utilities bills etc not counted sadly), as such it would take FOREVER to redeem another business class flight.

But weddings and moving into a new house constitute big expenditures (that you pray you wouldn't go bankrupt over). I am not going to talk about how ridiculous it is for people to spend nearly the same amount on weddings AND renovations. That's a topic for another day, or maybe not. People simply do not understand why it is unimportant to insist perfection on wedding day.

Ok maybe just one more time. Why? Why? Whyyyyyyyyyy

NOBODY CARES ENOUGH TO REMEMBER

So back to topic. Miles or Cashback?

For starters let's frame the typical scenario to:

a) $2500 for wedding gown package (inclusive of makeup)

b) $3000 for AD videography + AD photography - Cannot use card to pay, because most want internet banking or cheque. If your vendor allows card transaction yay for you

c) $30k wedding banquet that you cannot earn extra cash back because it is not under the "dining" category, too little ?! Please stop overspending

Ok never mind.

Tip 1: Listing stuff to do for wedding is very scary, because you would want to add more and more things. As I am doing the typical scenario, the stuff that I have left out include: prewedding photography, flowers, car rental, props, Instagram booth yada yada

FOR SIMPLICITY, let's assume you can charge $40k to the card.

This card is exceptionally good for those who DO NOT have a credit card with Citibank.

The promotional offer is insane. By paying $192.60 annual fee, you get to enjoy the bonus promotion.

Assuming you are spending all $40k in Singapore (where $1= 1.2miles), that's 48,000miles

If you can enjoy the 42k miles bonus, that's 90,000miles

A single round trip to Japan or Korea on business class cost 86,000 miles on SQ OR 80,000 miles on partner Star Alliance flight (think ANA with its bidet toilet seats, EVA air, Asiana Air). See I am being very nice, those who want to spend $40k+ on wedding usually want to go to atas place for honeymoon, so they can hao lian on Instagram. Japan is no US or Europe, but hey very good liao please.

Or if you are already a member, then the maximum you can earn by paying the annual fee would be 60,000 miles. Round trip economy class to Japan or Korea is 50,000 miles.

There are other miles card with high earning capacity but they often come with higher annual salary requirement and annual fees. At $50k per annum, this card is out of reach for people who are earning less than $4200 a month (no bonus, no AWS), so a similar more attainable version would be DBS Altitude, AMEX Singapore Airlines Krisflyer (that most basic, blue colour one) at $30k per annum. Also please reflect on spending $40k on wedding stuff if your earning power isn't that high.

That said a miles card has its obvious disadvantages:

1) You can only limit your redemption to flights or hotels

2) You get waitlist often for popular flight routes, planning way ahead to secure the seats may be hard for some

Tip 1: Listing stuff to do for wedding is very scary, because you would want to add more and more things. As I am doing the typical scenario, the stuff that I have left out include: prewedding photography, flowers, car rental, props, Instagram booth yada yada

FOR SIMPLICITY, let's assume you can charge $40k to the card.

Miles card

Citibank Premiermiles

This card is exceptionally good for those who DO NOT have a credit card with Citibank.

The promotional offer is insane. By paying $192.60 annual fee, you get to enjoy the bonus promotion.

Assuming you are spending all $40k in Singapore (where $1= 1.2miles), that's 48,000miles

If you can enjoy the 42k miles bonus, that's 90,000miles

A single round trip to Japan or Korea on business class cost 86,000 miles on SQ OR 80,000 miles on partner Star Alliance flight (think ANA with its bidet toilet seats, EVA air, Asiana Air). See I am being very nice, those who want to spend $40k+ on wedding usually want to go to atas place for honeymoon, so they can hao lian on Instagram. Japan is no US or Europe, but hey very good liao please.

Or if you are already a member, then the maximum you can earn by paying the annual fee would be 60,000 miles. Round trip economy class to Japan or Korea is 50,000 miles.

There are other miles card with high earning capacity but they often come with higher annual salary requirement and annual fees. At $50k per annum, this card is out of reach for people who are earning less than $4200 a month (no bonus, no AWS), so a similar more attainable version would be DBS Altitude, AMEX Singapore Airlines Krisflyer (that most basic, blue colour one) at $30k per annum. Also please reflect on spending $40k on wedding stuff if your earning power isn't that high.

That said a miles card has its obvious disadvantages:

1) You can only limit your redemption to flights or hotels

2) You get waitlist often for popular flight routes, planning way ahead to secure the seats may be hard for some

Cashback

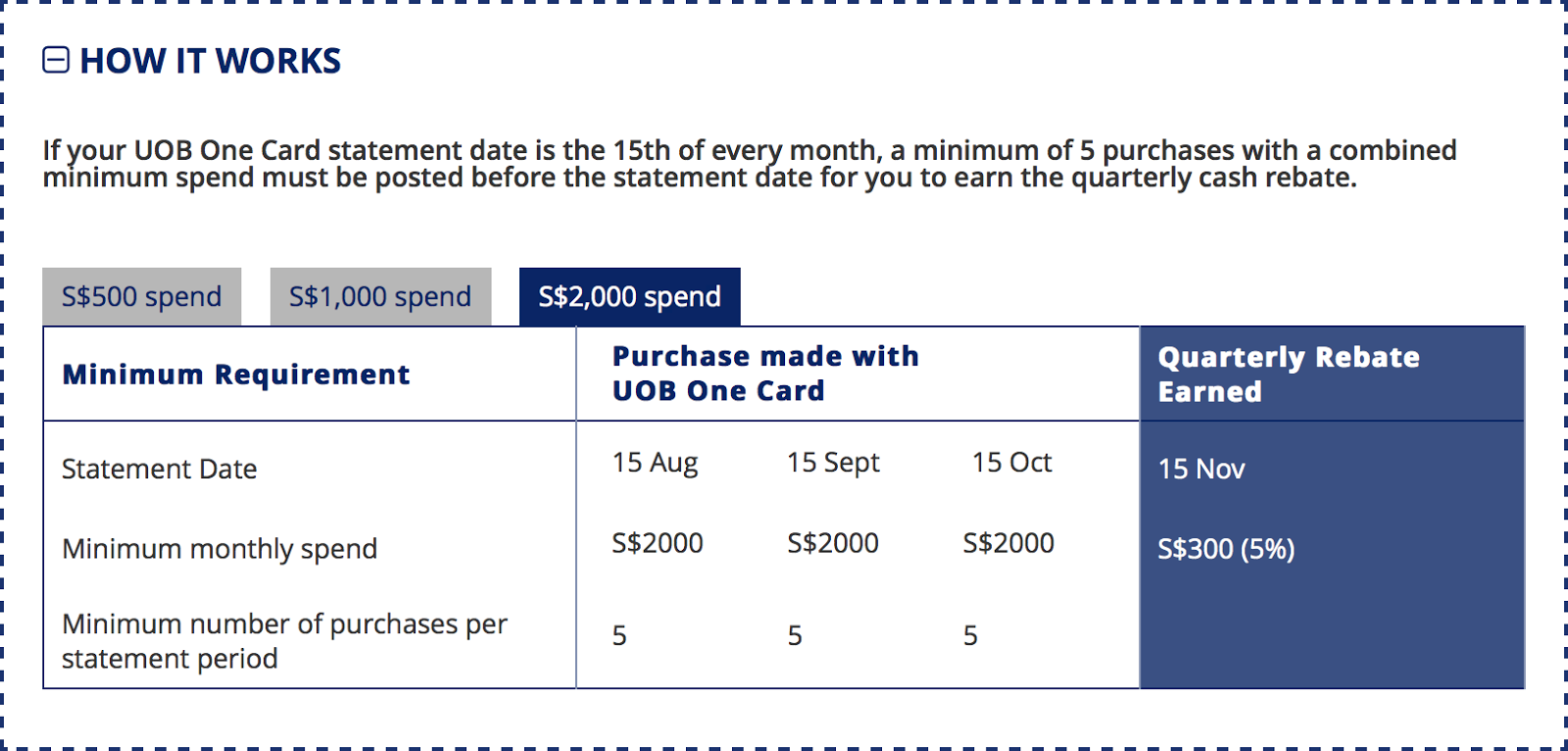

The obvious advantage of a cash back is that cash is king. With miles card you are limited to redeeming it for flights or hotels (not recommended) but cash goes anywhere. For the uninitiated, cash back does NOT mean that the bank gives you back the money in CASH, but as a credit to back to your card account and you can use that to deduct off from your monthly bills resulting in some form of savings.One of the favourite choice for Cashback is the UOB One card, as the bank has very smartly tie the interest rate of your corresponding UOB account to this. For simplicity, I am just going to assume that you only have the UOB one card, because estimating figures in bank account can go anywhere from negative to infinity.

The disadvantage of using cash back cards is that most banks puts quite a number of requirements in terms of spending. Generally, the more restrictive they are, the higher the cash back amount.

For example, some cards provide high cash backs for certain categories like dining ONLY or online shopping etc etc

Some require you to spend a minimum amount for each month in a quarter

Some require you to spend a minimum amount + minimum number of purchases.

UOB one card is the classic example of a card full of requirements.

If your wedding place allows you to pay back in instalment, then you may consider this card.

A $40,000 bill can be split into 20 monthly payments, also equating to 6.7 quarters. Netting you 6*300 =$1800 (there is no 0.7 quarter)

You would also need to make 4 other lame spendings probably at NTUC buying cup noodles, because too poor after wedding :P

$1800 can net you 2 economy round trip tickets to Japan or Korea and have some spare for Airbnb.

So this is probably a better card for those who are already existing Citibank card members.

The multiple requirements is probably the number 1 pet peeve for me, because there are so many things in life that are worth more of your attention than these. Some people would also use a mixture of cash back cards to try and earn more - that's when you will really get the wedding fatigue. Too many choices can tire people.

Overtime, banks tend to nerf cash back cards more than miles card, so you would probably have to keep shopping for a decent cash back card that suits your lifestyle more often than a miles card.

Examples include: Manhattan's cashback from 5% to 3%, OCBC Frank card, cutting cash back on online shopping from 6% to 3% and add a minimum $300 monthly offline spending (I will never forget this dick move OCBC), SCB Singpost card from 7% to 3% for online shopping and converting a miles card to cashback (HSBC). Miles cards are generally not nerfed because 1.2 miles per local $ is very sad already lah, please increase instead?

Ultimately, it really depends on what you value more, travel or cash for other stuff.

Have fun wedding planning :)

Ultimately, it really depends on what you value more, travel or cash for other stuff.

Have fun wedding planning :)

No comments: